The Bank of England has it warned That around 4 million households in the UK will face much higher mortgage payments, forcing the average homeowner affected by rising interest rates to pay nearly £3,000 more a year. This is due to the fastest consecutive hike in interest rates in three decades, which are designed to slow the economy and keep inflation in check. However, it is putting significant pressure on consumers who are already facing the greatest income pressure in generations.

The issue of higher mortgage payments has become one of the main contentions between the UK’s two main political parties ahead of the next election in 2024. Prime Minister Rishi Sunak’s government is looking at ways to ensure savers benefit from higher interest rates and to give borrowers more flexibility in restructuring their debts. For British households whose fixed rate mortgages expire, the monthly costs threaten to rise by hundreds of pounds a month.

“A full-impact rate hike is yet to come.”

The Bank of England has warned that it will be some time before the full impact of higher interest rates becomes visible, both in the UK and other developed economies. Although households and businesses are better able to deal with the problems than previous interest rate hikes, mortgage payment delays are now more common. This is because higher mortgage costs are now associated with a correspondingly higher cost of living.

The report also warned that owners of rental properties facing higher mortgage payments are considering selling their properties. This may lead to downward pressure on housing prices. Some landlords have taken out interest-only mortgages and are now raising rents to cover their higher costs. This has already increased rents in the UK.

Higher monthly costs

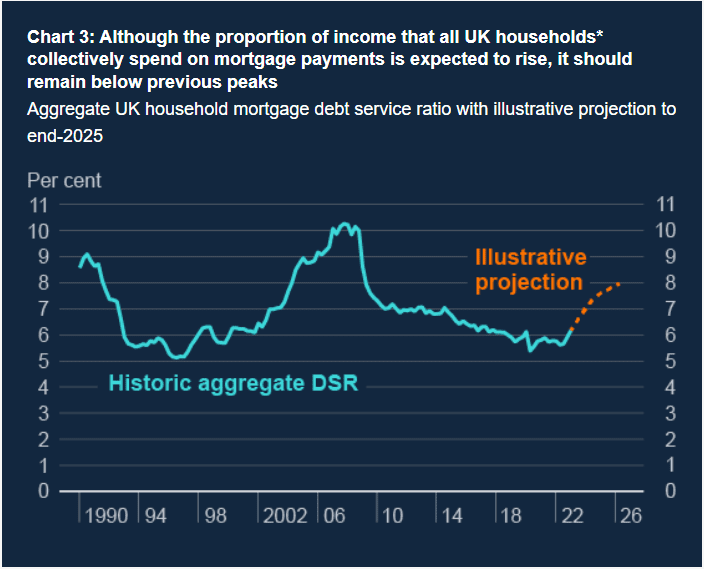

The total amount that households have to pay on mortgages is expected to rise to 8% of their taxable income by 2026. While this is higher than current levels, it remains lower than it was during the 2008 financial crisis and early 1990s .

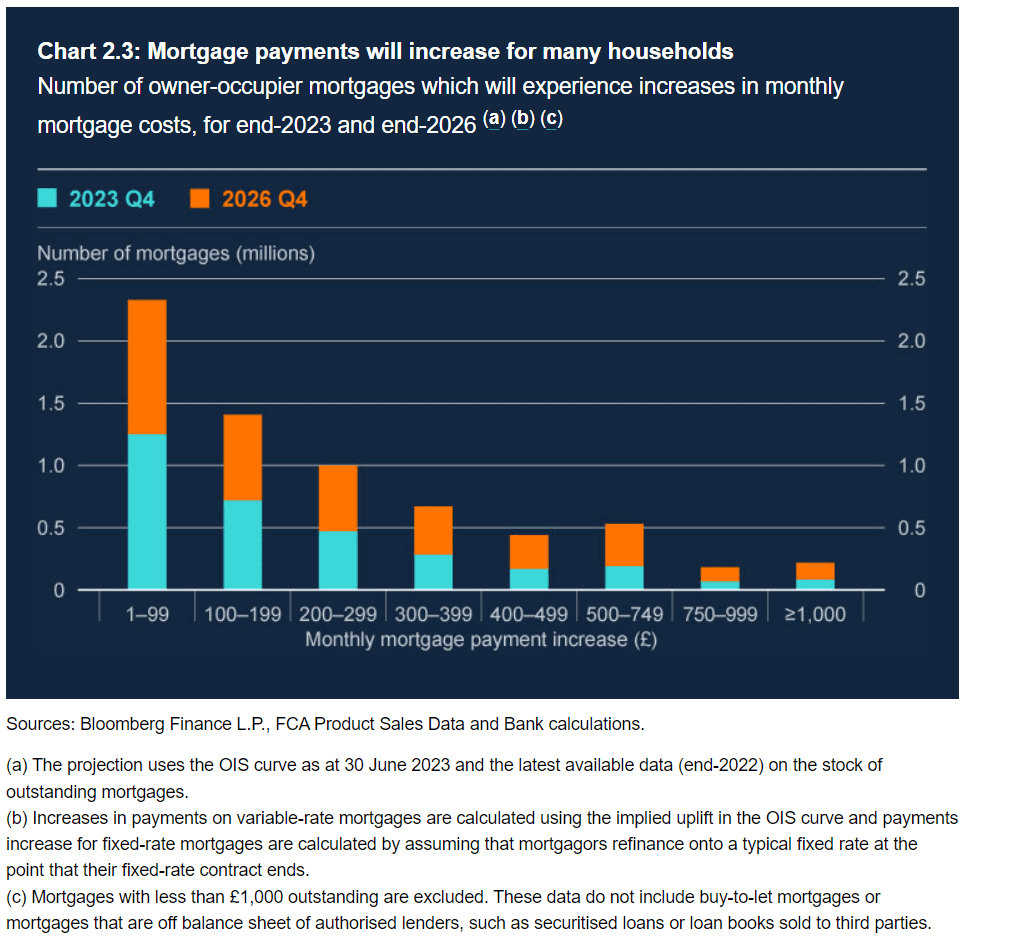

The Bank of England indicated that around half of all mortgage lenders have already entered into new loan agreements since the interest rate hike began in December 2021. However, it is important to note that the impact of higher mortgage rates has been delayed by the shift from variable rate mortgages to rate agreements. fixed for two or five years. In the past it was very common in the UK to take out variable rate mortgages, but this has become less and less in recent years.

UK house prices are expected to decline further as a result of higher mortgage interest rates and continued pressure on household real and disposable income.

Read all analytics on Geotrendlines starting from 1 euro, –